Bitcoin Eyes $100k | Gamma Squeeze

Friday November 22nd, 2024 - Issue # 89

(Any views expressed below are the personal views of the author and should not form the basis for making investment decisions, nor be construed as a recommendation or advice to engage in investment transactions.)

What a week. Congratulations to all of you on fresh all-time highs. If you’re new to this space, you’re probably feeling very excited. For some of us though, while we’re a hair away from 6-figure BTC, the feeling is something a lot less than euphoric.

I’ve been getting a ton of messages—people saying things like, “You must be having a good time,” or “Lucky for you!” Little do they know, they’ll likely be buying at much higher levels. Truthfully, the ones who think we’re “lucky” or assume we’re riding some wave of excitement weren’t here in the depths of the bear market.

They didn’t endure the pain from the blow-ups (FTX, BlockFi, Celsius, 3AC, Voyager, etc.), watch their banks get pulled out from under them during Operation Choke Point 2.0, or struggle to raise capital under brutal conditions. They pivoted to AI or went back to their “normal lives,” while we stuck it out, eating cat food and grinding through the tough times. So yeah, $100k feels...kinda meh.

Then there’s the other group—the investors who’ve been watching the market closely all year but couldn’t pull the trigger. They’re more sophisticated, long-term thinkers. But now, they’re caught in analysis paralysis. “No way we can buy at these levels,” they say. “We don’t buy all-time highs.”

I get it…but I don’t agree. In my opinion, we’ve just crossed the chasm. For the first time in history, Bitcoin is being taken seriously as the next world reserve asset. $100k is where we probably should’ve landed back in 2021 if FTX et al. hadn’t imploded, and the Fed hadn’t gone on a historic tightening spree.

At $100k, Bitcoin is still under $2 trillion in market cap—tiny in the grand scheme of things. For me, the recent price action isn’t a sell signal; it’s confirmation that we’re headed much higher. The asymmetry to the downside feels massively derisked. I’ve been buying BTC since 2017, and if I had any fiat left, I’d be excited to buy at these levels.

But enough about my feelings. I mentioned either last week or the week before that we were in for week after week of positive news. This week? Insane.

💡 Here’s an idea: instead of telling you all about it, I’ll let the screenshots do the talking. They say a picture is worth a thousand words, and these snapshots encapsulate just how wild things have been.

After that, I’ll dive into something I’ve been meaning to get smarter on—the new Bitcoin ETF options.

They say a picture is worth a thousand words…

Good riddance, Gensler.

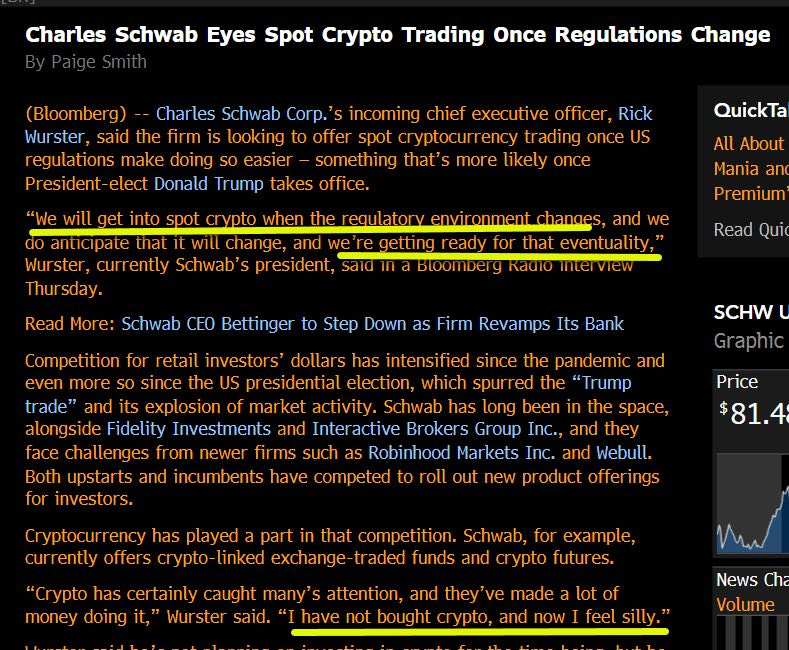

$9 Trillion Charles Schwab CEO: "I have not bought crypto, and now I feel silly." ..."We will get into spot crypto"

🤴Saylor with the largest ever Bitcoin purchase. Followed by another $3bn raise.

BTC takes Saudi Aramco for 7th most valuable asset. 5th spot is just a good week away…

Okay, this is starting to feel very real.

A bunch of corporations have added Bitcoin as a treasury reserve asset this week.

Marathon (MARA) raised $1 billion to buy more Bitcoin. Saylor playbook in action...

Speaking of Saylor, again — Saylor x Microsoft

This week the Shanghai court has affirmed that personal ownership of cryptocurrencies is legal in China, classifying them as virtual commodities with property-like attributes.

What else, what else…

Solana broke all time highs at $260

ETH

Trump Media files a trademark for “TruthFi” to offer digital wallets, crypto payments, and financial services.

Trump's DJT 0.00%↑ in talks to buy crypto trading platform Bakkt.

Bloomberg reported that Trump is considering creating the first ever White House Crypto role

Trump to meet privately with Coinbase CEO Brian Armstrong and expected to discuss appointments

All of this 👆 happened this week.

Bitcoin Options Market Explained

This week, Bitcoin ETF options launched—and I believe this could mark one of the most pivotal moments in Bitcoin’s financial evolution. These aren’t just another trading tool; they’re a gateway for both institutional and retail investors to engage with Bitcoin in a way that could fundamentally reshape the market.

What are options, and why do they matter?

Options allow traders to speculate on or hedge against price movements. A call option gives the holder the right to buy an asset at a set price in the future, while a put option provides the right to sell. For Bitcoin, options open the door for investors to gain leveraged exposure to its price movements with less capital upfront.

What’s groundbreaking is that these options are now trading on regulated U.S. markets, attracting institutional players who’ve been sidelined due to restrictions on offshore platforms like Deribit. This means that the “real money” investors—those managing large institutional portfolios—can now enter the Bitcoin derivatives market with confidence.

Why is this bullish?

Early trading data paints a compelling picture. Demand for call options (bullish bets) is overwhelming. The put-to-call ratio for long-dated contracts is hitting extremes of 1:10, meaning for every hedge against falling prices (puts), 10 calls are being purchased. This signals not cautious optimism, but bold positioning for significant upside.

Here’s where it gets fascinating: when market makers sell call options, they must hedge their exposure by buying Bitcoin as prices rise. The higher Bitcoin goes, the more they’re forced to buy, creating a self-reinforcing cycle known as a gamma squeeze. Bitcoin’s unique volatility—where sharp moves to the upside are just as frequent as sharp drops—makes this dynamic even more powerful.

Unlike traditional commodities like oil or gold, which can stabilize through increased supply as prices rise, Bitcoin operates with a fixed supply. There’s no mechanism to produce more Bitcoin to meet growing demand. This scarcity, combined with the leverage and accessibility options now provide, creates the potential for unprecedented price moves.

Why this is just the beginning

Consider this: in traditional markets, derivatives are 10–20x the size of the underlying asset’s market cap. For Bitcoin, derivatives currently represent less than 1% of its spot market cap. This massive gap highlights how underdeveloped Bitcoin’s derivatives market is—and how much room there is for growth. With institutional demand for hedging and allocation vehicles now fully unlocked, Bitcoin’s maturity as an asset class is about to leap forward.

While the potential for explosive price movements is exciting, it’s equally important to recognize the complexity these products add to the market. As the ecosystem matures, we’ll see how this impacts Bitcoin’s broader adoption and valuation. For now, it’s undeniable: Bitcoin is becoming a cornerstone of the traditional financial system, and this moment is one for the history books.

Till next week, friends.