Eat The Rich

Friday May 22nd, 2026 - Issue # 134

(Any views expressed below are the personal views of the author and should not form the basis for making investment decisions, nor be construed as a recommendation or advice to engage in investment transactions.)

Good morning to all of you still with me. I’ve noticed a decline in my readership and I think that’s a sign of where bitcoin is these days…boring (Homer Simpson voice)! To most anyway, but not I. One of the perks of writing these weekly missives is that I get myself bulled up to buy BTC even when it the market is so sideways. I typically end up market buying a 0.05 or .1 BTC on average — it would be hypocritical of me not to.

Last week was about why bitcoin is the best store of value and global settlement network at the nation state level. This week I want to bring it back to the plebs. The rich plebs that I think are crazy for not owning (real) BTC.

Wealthy people in the West are massively underestimating how obvious they’re becoming as the next political piggy bank. I’m not saying every government is going full communist tomorrow, or that everyone should panic, sell everything, and move to El Salvador (I’m also not, not saying that). But the math is getting ugly, and I don’t think the people with the most to lose are taking it seriously enough or they’re in pure cope mode.

Western governments are broke. Voters are angry, housing is unaffordable, young people feel locked out and scared, the middle class feels squeezed, debt is exploding, interest expense is eating budgets, defence spending is rising, and entitlement promises keep growing. Nobody has the political courage to admit the obvious: governments promised too much, spent too much, borrowed too much, and now the bill is coming due. So the easiest answer becomes: take money from the top 5% to make the other 95% happy (in the short term). A fool’s errand.

Doesn’t exactly fit but this was eye opening to me…young people drowning in college debt are shook that the piece of paper they’ve worked so hard for is about to be as valuable as a pile of Bolivars.

The message is simple. “The billionaires have too much.” “The wealthy need to pay their fair share.” “Unrealized gains should be taxed.” It sounds nice to most but it’s a very scary precedent.

For most of modern history, wealthy families optimized around normal stuff: tax planning, estate planning, trusts, real estate, private equity, and maybe some gold. The whole wealth management industry was built on the assumption that the system basically works. Banks, courts, currencies, even the government which was always annoying but not hostile and were slow to make changes. I’m not sure that’s the world we’re heading into.

The world we’re heading into feels more desperate, political, punitive, jealous, and “eat the rich” with government letterhead. When governments need money and voters are angry, they don’t go after the hardest thing to tax. They go after the easiest: the stuff they can see. Your house, cottage, brokerage account, private company, pension, trust, land, rental property, and estate. Visible wealth. Especially stationary wealth. Permissioned wealth that lives inside databases, custodians, banks, and borders.

Real estate is the clearest example. Everyone loves real estate until the government decides your house is a revenue opportunity with a roof. Property taxes, mansion taxes, vacancy taxes, foreign buyer taxes, capital gains changes, speculation taxes — the list grows. Real estate can be a great asset. Unfortunately I own real estate (want to buy my place? I’m offering a subscriber discount). I like real estate in places that I can’t afford, and countries like El Salvador where there’s more of an asymmetric bet on the future of the nation. But it isn’t sovereign. You cannot pick up your house and leave. Your house is sitting there like, “Hello government, I am wealth. Please tax me.”

The same goes for a private business. It can be an incredible wealth-creation machine, but it’s trapped in one jurisdiction: employees, payroll, licenses, audits, regulators, banks, and local politics. Most companies can’t be teleported offshore if the country starts treating successful entrepreneurs like an ATM. We’re seeing the ramifications in Canada right now where there is a massive amount of capital flight and entrepreneurs deciding to take their talents south of the border for better opportunities and a system that doesn’t come with as many headwinds. Sad.

Canada’s proposed capital gains hike in 2024 was a perfect example. The government tried to move the inclusion rate from 50% to two-thirds on gains above $250k for individuals, and on all gains realized by corporations and most trusts. For high earners in provinces like Ontario, that meant the effective tax rate on capital gains could push toward roughly 36%. That June 25 deadline became a line in the sand. We saw it firsthand with clients realizing gains and restructuring before the date. That was the nail in the coffin for a lot of people and we saw a number of our clients exit Canada because of it. It was dark days. Thankfully it didn’t stick, but it did its job if the goal was to force a massive brain and wealth drain and send a shockwave of distrust across the bow of ambitious Canadians. Unfortunately, there’s no doubt in my mind that we see more of this in the coming years.

Public markets feel cleaner on the surface, but your brokerage account is liquid only until someone changes what liquidity means. In Canada we have the TFSA and RRSP which are really great instruments to build wealth. For investors that take those vehicles seriously, you can build real wealth tax free or deferred in the case of the RRSP. We’ve actually had the opportunity to invest in paper BTC within our registered accounts since 2020 since Canada was one of the first countries to launch a publicly traded BTC investment fund. However, I’m not at all confident these sources of tax efficiency will be as they are in the future.

Capital controls, exit taxes, unrealized gains taxes, and wealth taxes sound scary but realistic (which is probably why they sound scary). The window moves slowly, then suddenly. California has a proposed 2026 ballot measure for a one-time 5% wealth tax on billionaires, payable over five years. I think it probably fails as Gavin needs to show some semblance of reasonability before he runs for the top job in 2028. However, I think it’s sadly another trial balloon and the Dems will be looking to normalize a wealth tax at the federal level as part of their campaign promise. I think the 2028 elections, just like the last few elections, are going to be the most important elections in our lifetime. It’s going to be very messy.

It’s already happening in Australia barring a dramatic change of events.

Australia’s Division 296 superannuation tax starts July 1, 2026, targeting balances above $3 million. The original version was going to tax unrealized gains, but they walked that back after the backlash. Still, it introduces higher tax rates on large retirement balances, starts measuring asset values more aggressively, and sets new thresholds for people who did the “responsible” thing and saved aggressively.

The UK replaced its non-dom regime with a residence-based system in 2025, narrowing a classic structure used by globally mobile wealthy families.

Whichever way you want to slice it, there’s no way in my mind that tax regimes in the West are going to become more favourable to the wealthy or ambitious citizenry. It might not get so much worse very quickly, but it ain’t getting better.

And so it goes…

Which brings me to gold, the shiny rock, the boomer bitcoin, the final boss of dinner table inflation conversations. I’m actually going to stay away from the weekly gold bashing this time because the letter is already long and I have barely mentioned bitcoin.

Gold works great…until you actually need to bounce.

Here’s the key distinction I want folks to understand: bitcoin exposure is not the same as bitcoin ownership. The ETF was obviously a massive milestone as it legitimized the asset class and opened the door for institutions, advisors, pensions, and every traditional investor who wants a ticker symbol instead of “internet money.” The ETF is convenient and useful and possibly a honey trap? I’m not here to dunk on it and I’m obviously biased as I would love for ETF buyers to buy real BTC through Satstreet, but it is not real bitcoin.

“Hey, this Bitcoin thing is really catching on. The train has left the station - it’s too big to kill now. Our only option is to push ETFs so the plebs buy the convenient version and never bother with the real thing. That way we keep their capital ring-fenced inside the system where we can still tax the shit out of it. We can’t risk them owning something so revolutionary they can actually store their wealth in their own heads if it ever comes to it.”

“It’s way too powerful.”

“Let’s call Fink and let him go to work on this.”

“The plebs will actually see this as a win!”

”Muah ahahahah”

-US Government

I’m not sure that’s how it really went down but I wouldn’t be surprised would you? The fact that you’re even thinking about that question means you need to sell some of your ETF exposure and give me a ring.

And no, I’m not advising you to evade taxes. Governments can and will tax income, gains, estates, corporations, residency, and transactions. They can make your life extremely annoying if they want to.

But here’s the part that actually matters: they cannot easily fence off the Bitcoin network itself.

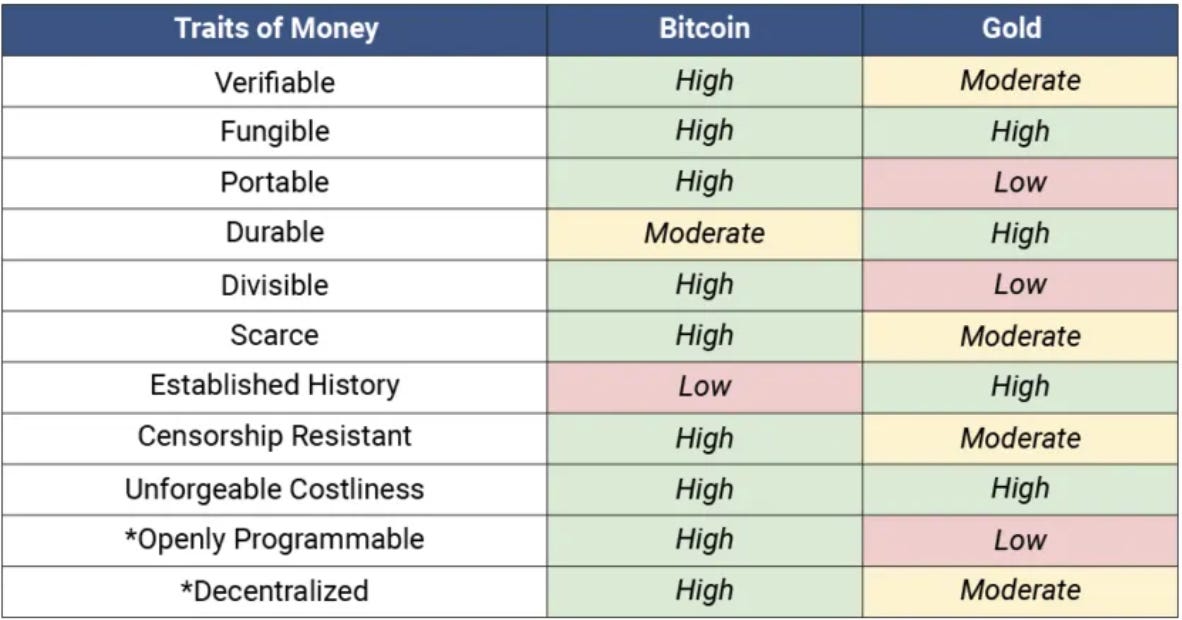

Properly held bitcoin is liquid, global, digital, scarce, and portable in a way nothing else is. It doesn’t sit in a database they control. It doesn’t need a bank, broker, or custodian to move. It doesn’t care what country you’re in, what time it is, or which politician just redefined the word “fairness.”

This is why the real question for wealthy families is quietly shifting. It’s no longer just “what is my expected return?” It’s becoming “what do I own that I can actually leave with if I ever need to?” “Is my plan B up to scratch?”

You can’t leave with your house.

You can’t easily leave with your private business.

Your brokerage account is liquid and available until it’s not.

Your pension and registered accounts are yours until the rules change.

Bitcoin sits outside that system. It is a different type of asset entirely and it should be studied thoroughly before being disregarded because you saw this video Michael Saylor put out yesterday. He really needs to stop with this.

Wealthy people already understand diversification: second passports, offshore accounts, trusts, assets spread across jurisdictions. Yet a shocking number still own zero real bitcoin. Even a modest 1–5% allocation in actual BTC (not just ETF exposure) can dramatically improve a family’s optionality. Call it sovereign insurance. Call it “just in case the people running the system are even worse at math than we thought.” Call it “schmuck insurance” if you want just don’t overlook it.

Custody matters, obviously. Real BTC is powerful but with great power comes great responsibility. Not your keys, not your coins. Lose your keys, lose your coins. Some wealthy individuals and families will use qualified custody, some collaborative custody, and some well-designed self-custody with proper inheritance planning and geographic redundancy. The details will differ by circumstance and technical capabilities.

Give us a call and we will help you with this stuff! That’s what we’re here for.

Bitcoin has to be treated as an asset that stands alone. If you own it correctly, it remains one of the only assets that can still move at size, globally, instantly, and without asking anyone for permission. Wealthy families in the West need to stop treating bitcoin like a weird tech trade and start treating it like serious sovereign infrastructure for their balance sheet.

I’m dead serious when I say this: having zero real bitcoin as a wealthy person or family in the West is irresponsible.

Real Bitcoin provides you with a level of optionality you can’t get anywhere else. And in the next decade, optionality is going to matter more than ever.

Have a nice weekend!